Managing the financial ecosystem of a Cooperative Housing Society (CHS) or Resident Welfare Association (RWA) in India has transformed from a simple neighborhood chore into a highly regulated, logistically complex operation. With modern updates to state-specific cooperative laws, stricter statutory tax compliance, and rising expectations from residents for absolute financial transparency, volunteer managing committees can no longer survive on paper registers, manual ledger updates, and basic spreadsheets.

This comprehensive guide serves as an operational blueprint for housing society managing committees, treasurers, and estate managers. It breaks down the intricacies of legal billing heads, the structural liabilities hidden within manual accounting, calculation protocols for defaults, and the precise application of statutory tax mandates to shield your society from penalties and resident trust deficits.

1. The Anatomy of CHS Billing: Breaking Down Maintenance Heads

A recurring point of friction in Indian housing societies is the lack of clarity regarding how maintenance bills are constructed. Managing committees often face resistance from residents who feel billed unfairly. However, a society cannot simply invent arbitrary billing structures; under modern model bye-laws (such as those governed by the Maharashtra Cooperative Societies Act), billing must be meticulously split into specific statutory heads.

Understanding these heads is essential for ensuring that collections are legally defensible and structurally sound.

Statutory Charges and Their Structural Benchmarks

| Billing Head | Calculation Methodology | Legal Cap & Purpose |

| Service | Shared equally across all flats, regardless of the size or carpet area of the apartment. | Covers operational overheads: staff salaries, security agencies, office administration, and common area cleaning. |

| Sinking Fund | Calculated based on a fixed percentage of the construction cost of each flat, excluding the land cost. | Set at a minimum of 0.25% of the construction cost per annum. This is a mandatory reserve strictly preserved for structural overhauls, major reconstruction, or unexpected structural emergencies. |

| Repairs & Maintenance Fund | Calculated based on a fixed percentage of the construction cost of the flat. | Set at a minimum of 0.75% of the construction cost per annum. Reserved for routine upkeep, lift maintenance contracts, pump repairs, and minor painting works. |

| Non-Occupancy Charges | Applicable only when a flat is sub-let or rented out to a tenant. Vacant flats or flats occupied by immediate family members cannot be charged. | Strictly capped at 10% of the Service Charges component of the maintenance bill. Charging any flat rate beyond this cap violates state cooperative laws. |

| Parking Charges | Fixed by the General Body based on vehicle type (Two-wheeler vs. Four-wheeler) and the number of slots occupied. | Rates are mandated uniformly across members based on allocation. Used to maintain parking lot infrastructure, line markings, and specialized security. |

| Utility Charges (Water & Common Power) | Can be distributed based on the number of water inlets/outlets per flat, or shared equally/by carpet area as decided by the General Body. Common power is typically distributed equally. | Pass-through costs derived directly from municipal water bills and state electricity board commercial meters for lifts and common area lighting. |

The Legal Mechanics of Area-Based vs. Equal Distribution

A common misconception among residents is that the entire maintenance bill should be tied directly to the square footage of their flat. The model bye-laws establish a clear division to maintain equity between small and large apartments:

- Equal Splits: Expenses that do not scale with the size of an apartment—such as security guard salaries, manager fees, stationery, and common area lighting—must be shared equally. A 3-BHK owner uses the security gate and lift infrastructure in the exact same manner as a 1-BHK owner.

- Area-Based Splits: Structural elements, such as the Repairs and Sinking Funds, scale with the physical volume of the asset. Therefore, they are calculated based on the built-up area of individual units. If a major structural column requires retrofitting, the larger unit holds a proportionately higher equity stake in that building structure.

2. The Hidden Costs of Manual Ledger Management

Many housing societies continue to run their entire financial operations via Microsoft Excel or legacy desktop software managed by an external neighborhood accountant. While this path seems cost-effective on the surface, it introduces systemic operational liabilities, leaves the managing committee vulnerable to personal liability, and drives structural trust deficits among residents.

The Problem with Fragmented Offline Tracking

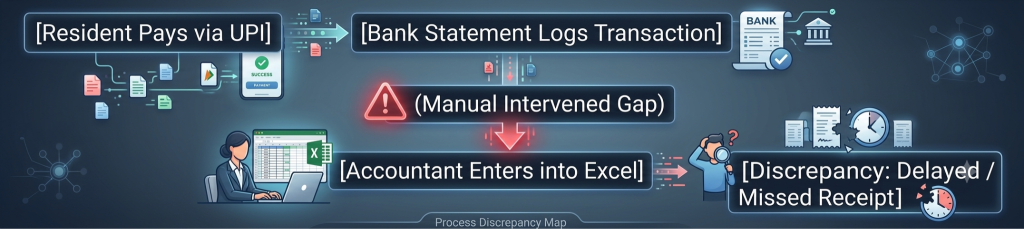

When a society relies on offline ledger management, data fragmentation is inevitable.

This manual intervention introduces multiple points of failure:

- The Reconciliation Gap: A resident pays their maintenance bill via NEFT/UPI and shares a screenshot on a messaging app. The treasurer forgets to log it, or the external accountant only visits once a month. In the interim, an automated or manual reminder is sent to the resident labeling them a defaulter, directly triggering a defensive and hostile relationship between neighbors.

- Formula Degradation: Excel sheets lack audit trails. A single accidental keystroke by a committee member can break a formula across 200 rows, leading to cumulative calculation errors in interest or opening balances that cascade over multiple quarters undetected.

- Lack of Read-Only Transparency: When financial books are locked on a single laptop belonging to the Treasurer, residents are kept in the dark. This lack of clear visibility breeds suspicion regarding the misappropriation of funds, even if the managing committee is working completely honestly.

Audit Failures and Statutory Rejections

Under the Cooperative Societies Act, every CHS must conduct an annual statutory audit through a certified panel auditor. Manual ledger management frequently collapses during this process due to:

- Voucher Mismatch: Physical payment vouchers often fail to match the dates logged in offline ledgers, leading to qualified audit reports.

- Improper Fund Segregation: Auditors look closely at whether collections for the Sinking Fund or Reserve Fund are being diverted into daily operational expenses due to poor cash flow visibility. Manual systems obscure this, leading to severe audit non-compliance notes.

- Inability to Track Historical Defaults: When flats change ownership, tracing historical dues across fragmented Excel files over a 5-year period becomes an operational nightmare, often delaying the issuance of critical No-Objection Certificates (NOCs) for property sales.

3. Automating Late Fee & Interest Calculations

Calculating interest on overdue maintenance fees is a primary driver of legal disputes within housing societies. Bye-laws grant societies the authority to levy Simple Interest on outstanding amounts to maintain healthy working capital, but doing this manually across dozens of unique ledgers is highly prone to errors.

The Mechanics of Legally Defensible Interest Compounding

According to modern revised model bye-laws, the maximum interest rate that can be charged on defaulted maintenance dues has been rationalized from historic highs of 21% down to a maximum of 12% per annum simple interest.

Crucially, this interest cannot be compounded. Charging interest on top of past unpaid interest is illegal under cooperative housing laws. The calculation must isolate the principal maintenance dues from the historical interest penalty bucket.

I = P x R x T

365

Where:

- I = Calculated simple interest penalty for the billing cycle

- P = Outstanding principal maintenance amount only (excluding past interest penalties)

- R = Interest rate per annum (e.g., $0.12$ for 12%)

- T = Exact number of days defaulted past the close of the grace period

Navigating Grace Periods and Due Dates via ERP Logic

A modern Enterprise Resource Planning (ERP) engine automates this logic down to the single day, removing personal bias or manual calculation errors from the equation. Consider the following operational sequence executed by an automated system:

1.Invoice Generation:Day 1 of Billing Cycle.

The system automatically compiles individual maintenance components (Service, Sinking, Utilities) and emails/SMSs a digital invoice to every resident with a unique payment link.

2.The Grace Period Window:Days 1 to 15 or 21.

A legally defined window (typically 15 to 21 days) where payments are accepted without any penalty. The system tracks incoming digital clearings and instantly reconciles matching invoices.

3.The Due Date Deadline:Day 22 (Cut-off).

The exact threshold hour where the invoice moves from “Active” to “Overdue.” Any payment received after 11:59 PM on this day is automatically flagged for penalty indexing.

4.Per-Day Interest Calculation:Day 23 Onwards.

The system runs the simple interest algorithm on the core principal amount daily. Instead of charging a flat monthly fine, it applies the penalty based on the exact day the payment clears the bank account.

By implementing this precise, rule-based approach, the managing committee can present an unassailable digital ledger to any resident questioning an interest penalty. This completely removes accusations of favoritism or administrative malice.

The Dual Threshold Test for RWA GST Applicability

An Indian Housing Society or RWA is legally required to obtain GST registration and levy tax only if it satisfies both of the following criteria simultaneously:

- The Aggregate Annual Turnover Test: The total revenue collected by the society across all heads (including taxable maintenance, commercial hoarding rents, and interest on fixed deposits) exceeds ₹20 Lakhs in a financial year (or ₹10 Lakhs for societies located in North-Eastern hill states).

- The Monthly Individual Maintenance Threshold: The specific monthly maintenance contribution collected from an individual member/flat exceeds ₹7,500 per month.

If a society has an annual turnover of ₹50 Lakhs but charges its members ₹6,500 per month per flat, zero GST is payable. Conversely, if a premium boutique society has an annual turnover of only ₹18 Lakhs but charges members ₹12,000 per month, GST registration is not legally mandatory because the annual corporate threshold has not been breached.

Navigating the Inclusions and Exclusions of the ₹7,500 Limit

When checking if a member’s bill crosses the ₹7,500 threshold, you cannot look at the grand total of the invoice. The government has clearly defined which specific components attract GST and which act as clean pass-through exemptions.

| Taxable Components (Counts Towards ₹7,500) | Exempt Components (Excluded From ₹7,500) |

| * Service Charges (Staff salaries, security, admin) | * Property Taxes levied by local municipal bodies |

| * Repairs and Maintenance Fund allocations | * Municipal Water Charges (billed at actual cost) |

| * Non-Occupancy Charges | * Common Area Electricity Bills (pass-through costs) |

| * Shared Gym, Clubhouse, or Pool Access Fees | * Sinking Fund contributions for future structural work |

| * Guard/Security surcharges and visitor passes | * Non-agricultural tax or state government land revenue |

Critical Rule on Entire Value Taxation: If a member’s taxable maintenance component crosses the threshold—for example, reaching ₹8,500—GST at the rate of 18% must be charged on the entire ₹8,500, and not just on the incremental ₹1,000 amount above the statutory cap.

Input Tax Credit (ITC) Rules for Housing Societies

While Residential Welfare Associations must pay 18% GST on inbound services (such as hiring professional security agencies, elevator AMC contracts, or purchasing common area LED lighting), they can leverage Input Tax Credit (ITC) to significantly optimize their tax outgo.

The GST paid to vendors for these operational inputs can be directly offset against the outbound GST collected from residents on their monthly maintenance invoices. However, to claim ITC legally, the society must maintain clean, digitized, and system-mapped invoices containing the society’s official GSTIN number. Manual tracking systems routinely drop the ball here, causing societies to lose thousands of rupees in unvouched tax credits every quarter.

5. Why onesociety Over Legacy Alternatives

When housing societies recognize the need to digitize, they often default to choosing one of two inadequate solutions: popular mobile applications built primarily for “gate/visitor tracking,” or archaic, desktop-based legacy accounting systems that require specialized training to operate.

onesociety addresses the distinct operational needs of cooperative housing finance, filling the massive functional gaps left open by these legacy alternatives.

The Problem with “Visitor-Tracking First” Apps

Many platforms dominant in the market were engineered from the ground up as security and visitor gate management tools. Their accounting features were added later as secondary modules. As a result, their financial backend often lacks compliance safeguards.

- Superficial Double-Entry Frameworks: Visitor apps frequently treat accounting as a simple list of cash-in and cash-out events. They fail to generate true corporate balance sheets, multi-layered trial balances, or separate capital asset accounting funds required by cooperative societies.

- The Payment Gateway Black Box: Gate-focused apps typically route member payments through generic, single-lane pools. This can delay the settlement of funds to the society’s actual bank accounts by multiple days, throwing off cash flow calculations.

- Lack of Bank-Grade Automation: These apps can send payment reminders, but they rarely automate the back-end ledger updates or match direct bank deposits natively without manual validation from a human administrator.

The Friction of Rigid Legacy Accounting Tools

On the other end of the spectrum are classic desktop accounting platforms. While mathematically sound, they introduce intense operational friction:

- The Single-Point-of-Failure User: They require a highly trained operator. If your society’s tech-savvy accountant or treasurer resigns or moves away, the entire operational memory of the society’s books leaves with them.

- No Resident Interface: Legacy software produces flat PDFs or printouts. Residents cannot log into an app to see their live ledger ledger history, download old receipts, or submit digital payment disputes. This lack of access keeps resident engagement low.

The onesociety Advantage: Direct Bank Reconciliation and Transparent Dashboards

OneSociety is engineered specifically as a comprehensive financial management ecosystem tailored strictly to Indian CHS bye-laws, offering deep automation where other options provide superficial workarounds.

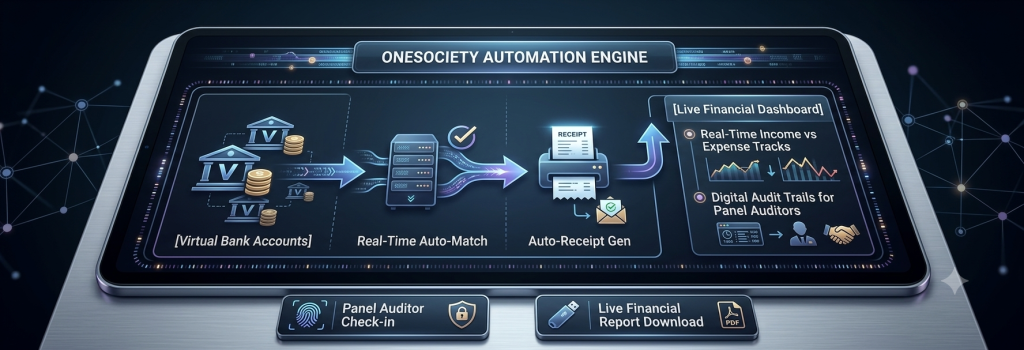

Automated Bank Reconciliation via Virtual Accounts: OneSociety allocates unique, virtual bank accounts (Van-Mapping) to every individual flat. When a resident completes an NEFT, IMPS, or UPI transfer, the payment hits their specific virtual node. The platform identifies the exact unit instantly, matches it against the open invoice, generates a digital receipt, and updates the society ledger in real time—all without requiring a human admin to review a bank statement.

Transparent Financial Dashboards: Instead of obscure balances, committee members and residents have access to intuitive, role-based dashboards. Treasurers can monitor live income-vs-expense tracks, cash-flow runways, and upcoming AMC contract renewals. At the same time, residents can review the health of the Sinking and Repair funds, keeping the neighborhood informed and fully aligned.

Auditor-Ready Compliance Engines: OneSociety generates system-mapped statutory ledgers, income and expenditure reports, and balance sheets that directly comply with the formats mandated by state cooperative acts. When audit season arrives, you simply provide your panel auditor with restricted, read-only digital access. This eliminates month-long manual cross-checking, keeps your books compliant, and protects your community’s hard-earned capital.

Conclusion: Future-Proofing Your Society’s Financial Legacy

Transitioning from the fractured world of manual spreadsheets and fragmented security apps to a dedicated, law-compliant ERP is no longer just a matter of convenience—it is a core governance obligation for modern managing committees. As Indian cooperative housing society frameworks grow more rigorous and communities expand, the legal and financial liabilities of mismanaged ledgers, inaccurate interest mapping, and missed GST deadlines fall directly on the shoulders of volunteer committee members.

By automating the billing lifecycle, housing societies can eliminate human error, secure their financial records against data loss, and build lasting institutional trust with residents. Platforms like OneSociety transform the arduous task of treasury management into a transparent, self-running, and fully compliant operation. Ultimately, effective financial automation does more than just balance the society’s books; it protects your community’s shared assets, preserves neighborly harmony, and safeguards the collective wealth of your housing society for years to come.